Back in April 2012, I wrote an article about what I thought was an estimate of the value of American Lorain Corp. (ALN) , the initial results were for a range going from 8.44$ to as high as 32.53$. Since then I revised down my estimate of the value of the company and I will elaborate on this point later.

First, let's examine some worrying facts. On October 15th Mr. Si Chen, chairman and CEO of American Lorain Corp submitted "a preliminary, non-binding proposal letter", in which he publicized his intention "to acquire all of the outstanding ordinary shares of the Company not currently owned by Mr. Chen at a proposed price of $1.6 per ordinary share, in cash, subject to certain conditions. Mr. Chen currently beneficially owns, in the aggregate, approximately 46.5% of the Company's outstanding ordinary shares."

A very disturbing fact about this proposal is that the independent committee that has been set up to analyze it, composed of Mr. Dekai Yin, Mr. Tad M. Ballantyne and Mr. Maoquan Wei; Mr. Yin as its chairman, is far from independent. In fact the independent committee held no shares in the company as of their last Form 3 filings according to the SEC, how can they related to the other shareholders of the company who have no influence on the company?

For the shareholders who have not read it, the official proposal letter can be found here. The Board will have to enter a delicate exercise to make sure they extract fair value for the remaining shareholders and that they do not unfairly disadvantage the shareholders other than Mr. Chen.

Using pretty much the same format used in my previous article, let's see how much this offer is ridiculously low compared to the current intrinsic value of American Lorain Corp.

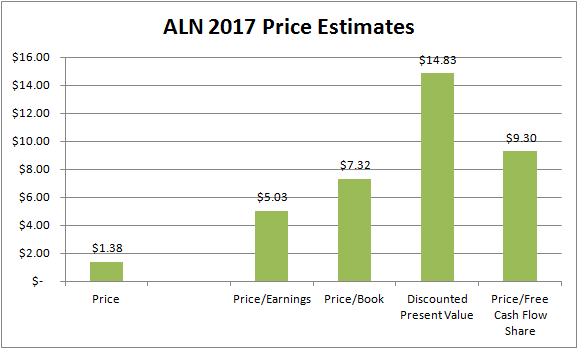

Assuming the current P/E ratio of 2.31, the current price assumes that the undiscounted earnings of American Lorain will grow by a little over 3% over the next 5 years, giving us a 2017 price of 1.60$, so the assumed figure of the CEO's proposal is actually lower. Public information tells us that earnings have been growing at about 24.8% a year over the past 7 years. Let's make another assumption that American Lorain is only able to grow EPS at 10% per annum. We find ourselves with a 2017 price of 2.35$ per share with the current P/E ratio. According to Reuters, the industry's average P/E stands at 34, but even with a ratio of 10 in 2017, American Lorain would be worth around 10$ per share.

From another standpoint, American Lorain has managed to grow its book value per share over the past 7 years at an average rate of 35% per year. Assuming the pace slows down to 20% as the company gets bigger, we end up with a book value of 13.58$ per share in 2017. If we use the current incredibly depressed Price/Book ratio of 0.26, we end up with a price per share of 3.53$. If we compare once again to the industry, we see that the average Price/Book ratio is close to 5. Using an alarmingly conservative Price/Book ratio of 1 for the year 2017, we obtain a value of 28$ per share.

Finally, as of June 30th 2012, the book value of the company amounted to 4.79$ per share, which is a 245% premium over the closing price as of October 15th 2012, or a 316% premium over the referenced October 8th closing price. The Board therefore should categorically reject the offer. Accepting the offer would be a blatant case of conflict of interest and negligence of the right of shareholders that are not insiders. Mr. Chen must have insulting levels of chutzpah to try to acquire a company he knows currently incredibly undervalued.

(click to enlarge)

In my opinion, if they intend to accept the offer, the Board could still give at most a 30% discount to Mr. Chen and offer shareholders a meager 3.35$ per share, this would be less insolent. His attempt is clearly an insult to the intelligence of the company's shareholders. I still err on the side of the book value of the company as a starting offer to shareholders.

Disclosure: I am long ALN. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.