At the time of this writing as well as at the end of the year American Lorain Corporation represented slightly over 50% of the whole portfolio. Just to recap, here is an excerpt from last year's letter on why I am so heavily invested in Chinese Reverse Merger companies.

At the end of 2010, an accounting scandal of incredible proportions was affecting the sphere of Chinese reverse merger companies. Investors were relentlessly dumping their share holdings on the market and all companies related to china saw their share prices prices fall over 70%.

ALN is one of the falling knifes I was able to catch right. Let's hope I did it before it hit the ground. At the time of writing this article on 23/02/2015 after market close, the company's stock has already returned over 32% year to date. I am convinced that more impressive gain s still remain to be harvested over the next two years.

There are also a few blunders to mention. Guanwei Recycling Corp. is one of the reverse mergers that burned me for the year. If it was not for that company, my performance for the year would have hovered around 0% for the year. This would have been acceptable considering that ALN, my main position, is still consolidating.

Biglari Holdings Inc, formerly know as (Steak n Shake) is the new addition for the year. A small position was opened just to follow and understand what the company's Chairman, CEO and biggest shareholder, Sardar Biglari is trying to build over time.

Here are my positions for the year:

Long:

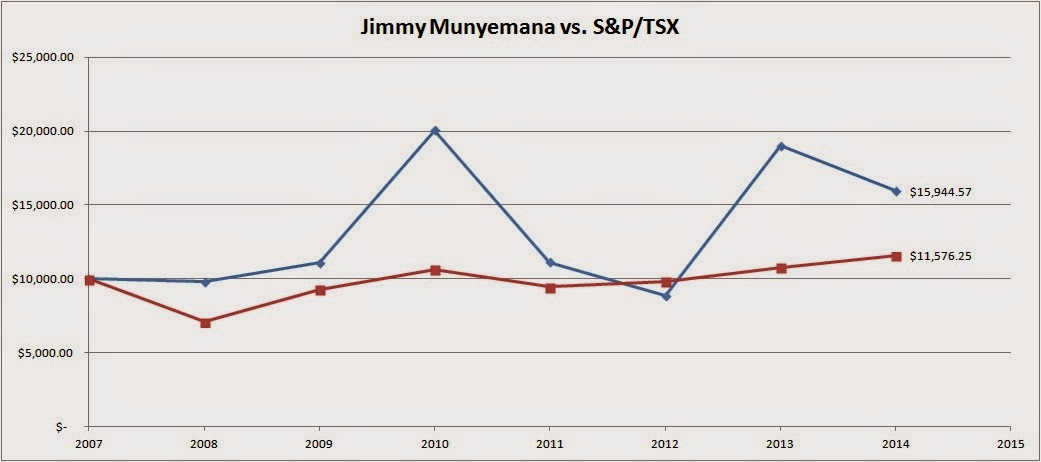

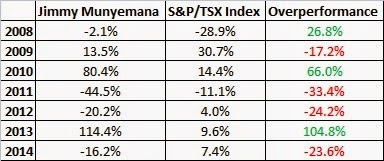

Taking those positions into account, my performance in 2014 was a disappointing -16.2%, and the S&P/TSX did 7.4%, so it makes it that I under-performed it by 23.6%. This is very in line with that I should expect with my level of experience in that market. Last years performance was likely due to chance and it is very improbable that I will be able to replicate it in the future.

Previous Years Performance:

2013

2010

2008

Previous Years Performance:

2013

2010

2008